ANNUAL REPORT ‘12

ECONOMIC AND REGULATORY ENVIRONMENT

31

despite the crisis, international tourism surpassed

one billion passengers, the highest number ever.

According to estimates by the World Tourism

Organisation (WTO) international air transport

will grow by 5% in 2012, boosted by the growth of

international traffic in the Middle East and Latin

America. Domestic air transport is expected

to decrease, with China being the only economy

that continues to have strong growth in that

market.

The figures for air freight are not as encouraging, with

declines being recorded for the second straight year.

This trend is explained by this sector’s heavy depend-

ence on the macroeconomic situation and develop-

ments in world trade, which is now concentrated on

emerging economies more than on those of the USA

or Europe.

This environment of strong competition between

airlines, associated with the change in their business

models and in air transport trends, has placed growing

pressure on airport operators. The adaptation of air-

port infrastructures to make them more efficient with

a lower operating cost has been one of the market

requirements. One illustration is the way low-cost

airlines burst into the market. Infrastructures had to

be adapted to their needs, in particular to be able to

respond to the shorter turnaround times of the

aircraft, which is characteristic of their operations. But

many of these companies chose to operate in second-

ary airports, or at old military bases, bringing into the

market airports that had been practically unknown

until then, like Tampere in Finland, or Zaragoza in

Spain.

This has increased the competition between airports

to capture new routes and new passenger flows, while

at the same time there is greater pressure from the

airlines to reduce airport fees.

Airport operators have been forced to come up with

differentiating factors, and the need to pay more

attention to airport marketing is an inescapable reality.

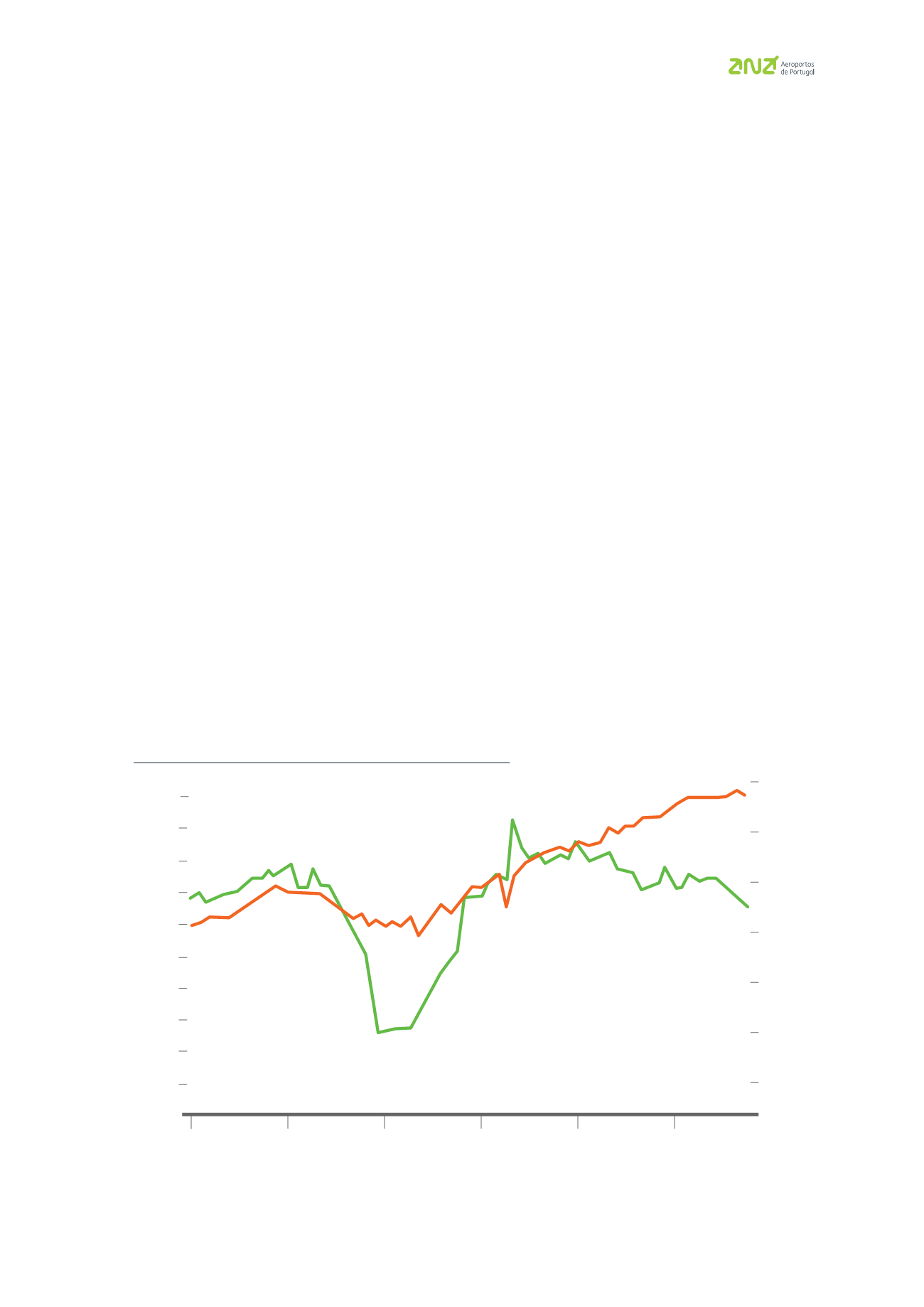

RPKs

FTKs

Source: IATA

450

430

410

390

370

350

330

310

290

270

2007

2010

2009

2008

2011

2012

TOTAL AIR TRAVEL AND AIR FREIGHT VOLUMES – Seasonaly adjusted

RPKs per month (billion)

FTKs per month (billion)

17

16

15

14

13

12

11