ANNUAL REPORT ‘12

ECONOMIC AND REGULATORY ENVIRONMENT

30

attract more and more passengers.

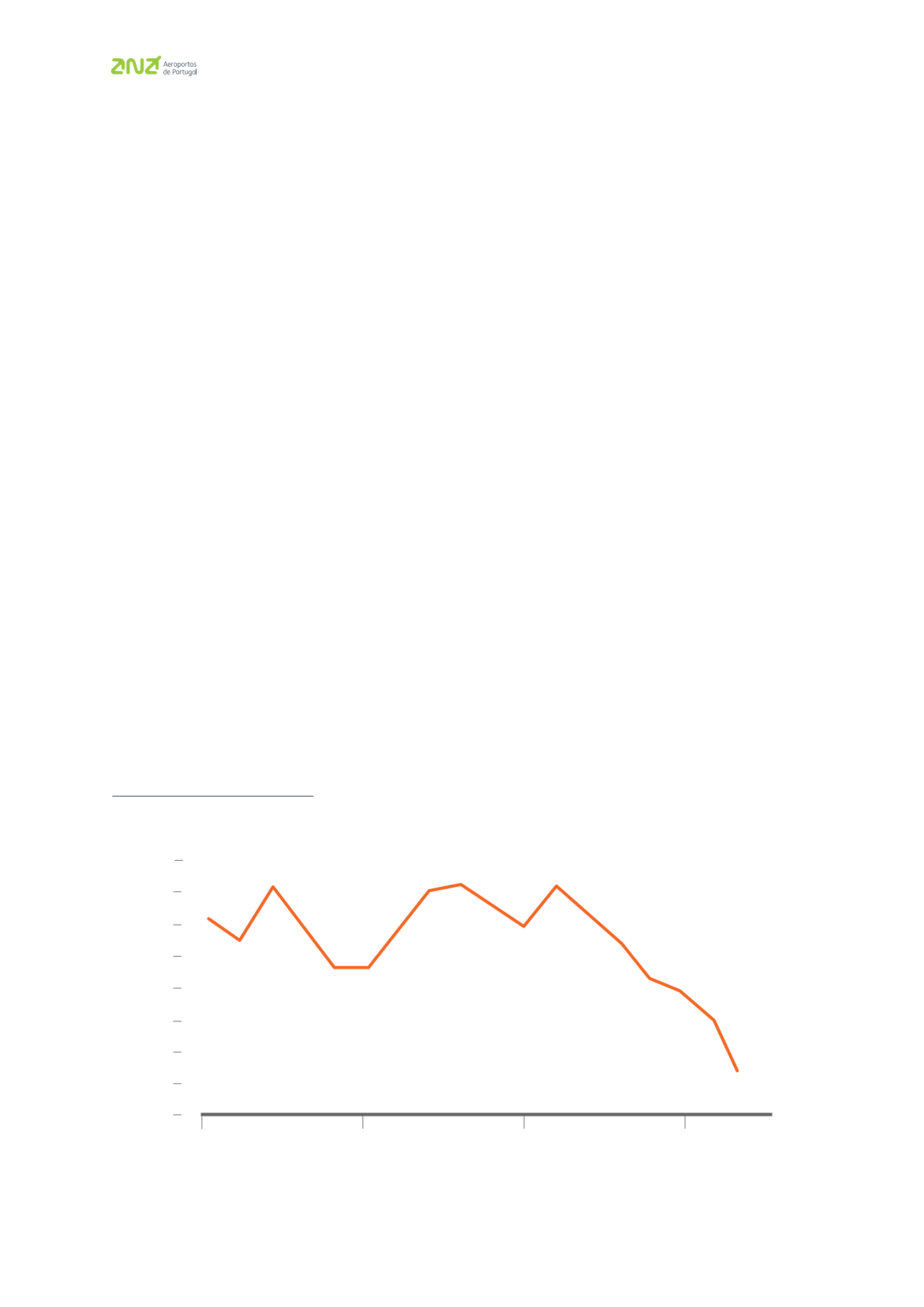

In spite of this trend, the number of low-cost air

carriers decreased in 2012 (especially in Europe), with

only the strongest companies being able to survive and

in the process improve their performance. The number

of new airlines has also decreased, a reflection of the

growing difficulty in obtaining financing for new invest-

ments.

The so-called traditional companies have been

forced to respond to these challenges through

consolidation and increased negotiation powers of

their alliances. Examples include the Continental-

United merger, the purchase of BMI (British Mid-

land International) by IAG (International Airlines

Group) and the possible merger of American Airlines

and US Airways.

Additionally, many of these airlines have revised

their business model, to adapt to new market

trends and have created their own low-cost airlines.

Examples of this strategy are Lufthansa, with its

Germanwings, IAG and its holdings Vueling and

Iberia Express, and the AF/KLM Group and its

subsidiary Transavia.

In the medium-haul sectors the biggest concern of

European airlines has been the competition from

low-cost airlines, but the long-haul carriers are

also under growing pressure from the exponential

growth in capacity offered by the so-called Gulf

airlines (Emirates, Ethiad and Qatar), which offer a

quality product with strong support from their

States.

Consolidation and restructuring: these are the

primary reasons given for the increased efficiency

in the air transport sector and, subsequently, for

the retention of earnings they have been able to

achieve in the face of rising costs. IATA revised its

projections upward for profits of the global aviation

industry for 2012, forecasting profits to the tune

of 6.7 billion dollars, over twice as high as it had

anticipated in June (three billion).

With tourism as one of the main motives for air

travel, it is equally interesting to note that in 2012,

Source: Ascend

160

140

120

100

80

60

40

20

0

1995

2005

2000

2010

NUMBER OF NEW AIRLINES FORMED